The theory of economics explains the increase in repo rates as a step taken by the government to curb what citizens are spending on an everyday basis. The step is usually taken to help control inflation. The theory is simple - increase the interest rates so that people refrain from opting for expensive loans, control their spending, and hence, curb inflation. The Government of India, and the Reserve Bank of the country, however, might have missed one aspect (or they may have not) before announcing the increase in Repo Rates - there is CoronaVirus induced revenge shopping taking place in all parts of the world!

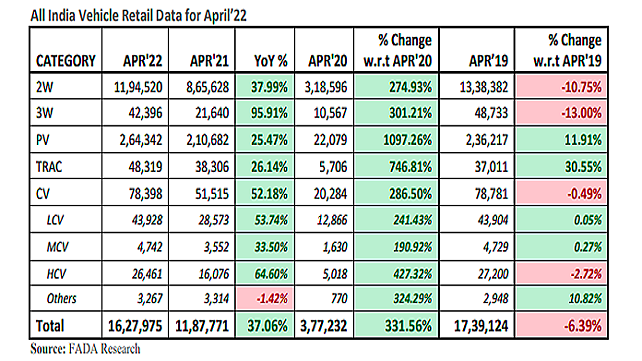

One more data point worth mentioning here, keeping India's automobile industry in focus, is that the industry's sales figures have started picking up pace, matching those prevalent before the pandemic. Though the numbers are still a little less when compared with those of 2019 (see chart below), these new numbers have ignited hope once more in the industry. Despite the banks and NBFCs having the privilege to disburse loans at interest rates based on the CIBIL score of their customers, it cannot be denied that the automobile industry will take a dent, even if minor, because of the recent Repo Rate hikes.

As Vinkesh Gulati, President of FADA, put it, 'The RBI's move of increasing the rep rate by 40 bps has clearly taken everyone off guard. This move will curb excess liquidity in the system and will make auto loans expensive. Certainly, this move will apply certain amounts of brakes on auto retail and dampen the sentiments further.'

Impact On 2Ws: Backbone Of India's Automobile Industry

The 2W segment, considered to be the backbone of India's mobility sector, might not be able to take one more blow. The 2W market, as Gulati explained, has not been performing due to an increase in fuel prices, a hike in rates and an underperforming rural market.

'The major impact will be on the entry-level segment of two-wheelers as it is already under a lot of pressure. That is where increased instalments even by INR 100 or INR 200 will make a difference. Practically we will now have to wait and watch how much hike does the banks and NBFCs do,' noted Gulati.

The FADA President is of the view that even if the banks and NBFCs absorb the hike, the announcement of an increase in repo rate will dampen the spirit of the two-wheeler market. About 70% of the total vehicles sold in India, as per FADA, are sold through finance. Many people who had earlier postponed their two-wheeler buying, as per Saurav Kumar, MD, Protiviti Member Firm for India, might continue to do so because of the increased interest rates.

'The country's automobile sector is largely driven by financing. A large part of people look towards loans when it comes to buying two or four-wheelers. The impact would be bigger on the two-wheeler market because the segment has already been struggling due to corona-induced consumer sentiments,' argued Kumar.

Total automobile sales in India in FY22 stood at 16,375,799 units, with the two-wheeler segment contributing 73% of that with total sales of 11,973,415 vehicles. It was in FY19 that the industry had seen peak sales of 22,467,808 units. Even then, two-wheelers had accounted for 76% of the overall sales with 17,118,332 units.

Fewer Cars Or No Cars

India's four-wheeler/passenger vehicle category is already in a dilemma of high demand and low supply metrics. Waiting periods for certain cars (like Mahindra Xuv 700) have exceeded more than a year due to supply chain constraints.

Kumar said, 'This sudden increase in repo rates will further dent people who are looking to pick up a car. There might also be cases of people cancelling bookings of cars owing to higher rates of interest as people may not be willing to pay extra.'

In numbers, a 10% interest on INR 1,000,000 car loan spells paying INR 100,000 interest in a year, whereas a 2% increase in the rate would mean paying an additional INR 20,000 interest every year.

As per Atul Chandel, Director Autobei Consulting Group, car purchase decisions will not change or get delayed. Individuals, however, will now choose lower variants of cars that they are interested in. They will do so to absorb the rise in payments and EMIs they will be making. He is also of the view that the luxury car segment is too niche to feel the impact of the increase in interest rates.

An individual associated with one of the leading private banks of India, on the condition of anonymity, noted, 'There would be negligible impact on the two-wheeler sales as the interest rates won't make much of a difference. Also, as the two-wheeler sales are dipping, end consumers will always have an option for negotiating with the dealers and OEMs. I think the larger effect will be seen on the four-wheeler market. There would also be absolutely zero effect on the commercial vehicle market minus the tractors.'

No Impact On CVs

The commercial vehicle category, encompassing trucks, cargo three-wheelers and more, might not feel as significant an impact due to the increased rate of interest on loans as the other categories. This is because, unlike the passenger cars segment, where most of the buying takes place for personal commute or leisure, commercial vehicles are primarily sold out of the need for transporting something from one place to another.

'More than 95% of CVs are sold through the finance medium. There might be an impact but it will not be big as CV buying and selling are directly related to the economy of a country. The retail will only get affected when the economy gets hit,' argued Gulati.

As per all the consultants Mobility Outlook spoke to, there will be no impact on the CV sector as it is generally regarded as a Capex investment by the buyers. However, the proof of the pudding lies in the sales data posted by the commercial sector. The PV segment posted 25.47% growth YoY in April 2022. This is, as a matter of fact, one of the only two automobile segments that posted growth even when compared to April 2019 figures. In April 2021, a total of 210,682 PVs were sold.

'Increases of any kind in prices in the CV category, whether taxis or trucks, can be easily passed on to the end consumer. Whether it is fuel cost, State or Central tax or bank interest rate, commercial segment always passes on the cost to end-consumer as it is a necessity,'

Plan B For OEMs/Dealers

While it is a wait-and-watch game for the OEMs and dealers, as only a few national banks have announced a hike in the interest rates, the former, as per Gulati, will have to tighten their socks and apply out-of-the-box strategies to tackle the challenges that may arise. The easy way out of dealing with a hike in interest rates (if all private banks do so) could be in the form of announcing aggressive schemes and discounts on vehicle buying.

'Supply chain is also an issue with the two-wheeler dealers at the moment. Most of the dealers of HMSI, Bajaj or Hero are sitting with inventories for more than 20-25 days. With HMSI announcing a 100-cc bike, things will heat up once again in the domain. It would be interesting to see what strategy the OEMs and dealers follow if in case sales of 100-cc bikes increase, and there is also an increase in the interest on loans,' Gulati said.

An increase in repo rates is usually the first step a country takes to control inflation. Commodities become a bit dearer when it comes to the spending power of individuals. There, as per Kumar, are many more things which need to be done on an overall level to bring inflation down. 'This is Economics 101 that you make things expensive, and people will help bring inflation down. The step is in the right direction, but we will have to wait and watch how the future unfolds,' shared Kumar.